Strategic acquisitions have a historical failure rate of 70-90%. That’s a pretty dismal stat.

So, what are you doing wrong? And, more importantly, how do you properly lead your team in an acquisition process when the cards are stacked against you?

Below are five of the most common mistakes we see corporate buyers make when going through the acquisition process. These mistakes can be costly – especially, if the deal dies after you chased it for months. We’ve included reminders of basic, yet vitally important, acquisition principles that will allow you to steer clear of failure and action items to help your team gain momentum in the right direction.

How Corporate Buyers Kill Deals

1. Not thinking strategically

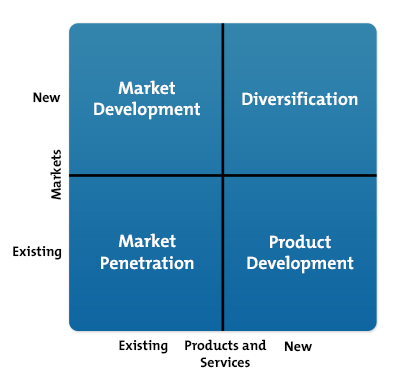

In over 13 years of mergers and acquisitions, we’ve only once seen a company produce a Sustainable Growth Matrix, let alone actually use one to guide their acquisition strategy. Where does an acquisition fit into your strategic plan? How does an acquisition serve your goals?

Our client, Alphapointe has made two acquisitions (Matchless Molding and Proformance Calling). As a nonprofit, acquisitions of private businesses are unique, with many nonprofit organizations completely unaware of this option. Alphapointe made this innovative decision through very strong strategic planning. Their acquisitions furthered their mission of employing blind or visually impaired people, dramatically improved the performance of their historical investment portfolio, and allowed consolidation into their current facilities for synergy gains. The acquisitions diversified their revenue into private-sector contracts and into new products being sold to new customers. Their strategic acquisitions were strategic at multiple levels.

Action item

Dust off – and upgrade – your strategic plan. Don’t have one? Create one. If you’re really feeling froggy, unchain those newly minted MBAs and let them use their education to create a Sustainable Growth Matrix for you to uncork at your next board meeting. This is time well spent – strategy is the foundation of a successful acquisition.

2. Not being ready to make decisions

Acquisitions are full of decisions – large and small, in real time and, often, with short notice. Without an internal system for decision making, any acquisition process gets bogged down. And time will eventually kill all deals. Be asking these questions:

- Who are your decision makers, at the various levels, as prospects filter through the process?

- How will you maintain momentum on multiple simultaneous deals?

- Who is the dedicated point person accountable for key communication to the acquisition team?

One of our more successful clients maintains an internal point person to act as project manager for their management team, with 30% of their workload budgeted to the acquisition process. That may not sound like a lot but it makes the process much smoother. Although not the final decision maker, being in close and continual contact with this person gives us insight to better understand dynamics within the company. Collectively we can immediately engage the proper people depending upon where an opportunity fits within the strategic plan so we don’t lose a great prospect to inattention or a faster competitor.

Action item

Create an internal deal team and task one person to lead. Assign specific roles to each team member with clear expectations about how much time each person is expected to invest in the process. Explain the hierarchy of communication and the gating mechanisms that will demand their attention as prospects move through the funnel.

3. Thinking too narrowly

Did your MBA finish that Sustainable Growth Matrix yet?

You must have an investment thesis. Define various quantitative and qualitative criteria for a successful acquisition, and then give yourself the latitude to achieve that success in multiple ways. Flexibility gives you options. Stick to – but continually evaluate – your thesis. Industries cycle, so don’t get caught in the trap of overspending on an acquisition or closing a cancerous cultural fit because you are only pursuing the ‘More To The Same’ quadrant because “That’s what we know.”

Yes, many of our strategic buyers have pretty specific desires for their acquisition. These desires, like existing equipment, facility, customer base, specially-trained employees, etc., allow for quick analysis and filtering of acquisition targets. Targets that achieve geographical expansion or market consolidation are the usual suspects. But, what if the usual suspects are too expensive, simply not available or the last company you would ever want to buy?

Take a step back and ask – “What COULD be my criterion for success?” If you’re going to dedicate the time, energy and money to run a process, then run a real process. Leverage the expertise of your outside resources and run them ragged. Open that throttle wide and see if you can find that Blue Ocean acquisition. Even if you don’t get to a Blue Ocean, you’ll still have the usual suspects in the funnel to close.

Action item

Fill out this workbook to help you begin developing a flexible, diverse investment thesis for success.

4. Forgetting that marketing matters

Targets will respond to your brand and your approach– the targets may be curious, flattered or confused about why you reached out to them. It doesn’t matter, as long as they respond. Particularly for closely-held businesses, if you can’t elicit any emotion out of the target, your response rate will be minimal and acquisition success plummets. Be thoughtful about how you’re positioning yourself.

When we reach out to target companies on behalf of our corporate clients we include a profile of the business – including an overview, history and acquisition objectives. This is where a target business owner’s interest is piqued. Even if they haven’t heard of our client’s company they might be impressed with the positioning and their interest grows when they do a little research. We’re continually refining our process – our efforts have produced a 8-24% response rate. Sellers want a trustworthy buyer, to feel like the inquiry is sincere and professionalism exists if they decide to respond.

Your reputation matters and your approach is critical.

Action item

Answer these questions (and then make adjustments if the answers aren’t satisfactory):

- What is my company’s reputation in the industry?

- How will a target respond to outreach with my company’s name on it?

- What will they think about my company when they look it up online?

- Will I survive a Google search? Or more importantly, the quiet, strategic calls made to find out if the solicitation is legitimate?

5. Not thinking about the financial finish line

You must be ready to execute financially. Making an acquisition is expensive. Making a bad acquisition is even more expensive. Going “0-fer” after 24 months is expensive and painful.

You must be ready to execute financially. Making an acquisition is expensive. Making a bad acquisition is even more expensive. Going “0-fer” after 24 months is expensive and painful.

Where is the money coming from to close your acquisition? Our DVS Murphy’s Law of Acquisitions states that you will always find a dream acquisition that sits 25% outside the boundary of the highest limit you defined in your investment thesis. Or, the combination of growth rate, competitive pressure, assets involved, negotiated terms, etc. completely mangle the capitalization structure your CFO and bank designed for the investment thesis. Where is the money coming from for the deal you want, but you can’t close internally? External capital partners have different requirements. Think about how your investment partner will impact your operations.

Our corporate clients establish their outside transaction size boundaries for their process, and many inevitably uncover a few that follow DVS Murphy’s Law. The siren song of that ideal target is so strong, and we find ourselves fighting to force our clients to maintain discipline with their investment thesis to keep them from eventually crashing on the rocks.

Our disciplined clients avoid those crashes because we discussed the eventualities of a deal too big. The options are:

- Walk away

- Stretch and get comprehensive organizational and board buy-in to go ahead and eat the whale

- Navigate a joint venture

- Completely change banking relationships to a larger bank

- Quickly bring in outside capital from mezzanine, mequity©, or equity investors

Financial agility calls for special expertise – it can resurrect a deal or save you from the wrong one. If you aren’t ready to pivot quickly, your acquisition will get run over by time.

Action item

Understand exactly what your financing limit and structure limitations are for your current bank, define your absolute limit of equity investment, and have your acquisition team learn what outside capital looks like for an outsized deal.

—

Sometimes what’s left undone is what kills a deal. Failing to think strategically, having a poor communication and decision-making structure, operating out of an inflexible investment thesis, forgetting about the response you elicit in the market, or not having a plan for the financial finish line are deal-killing mistakes we’ve seen corporate buyers make.

Those mistakes are part of the reason strategic acquisitions are cursed with a 70-90% failure rate. But there’s no need to be spooked. Follow through on the action items included and maybe you can avoid that curse.